Pipit Global is working to bring down the cost of remittance around the globe in line with the UN target of 3% fees by 2030.

In 2019, an estimated $550 bn (USD) was sent overseas in remittances. The top five remittance recipient countries were India (83.1 bn), China (68.4 bn), Mexico (38.5 bn), The Philippines (35.2 bn), and The Arab Republic of Egypt (26.8 bn) (World Bank, 2020)

2020 saw a reduction in global remittance flows to $508 bn as one of the negative impacts of the global pandemic as lockdowns and travel bans hindered migrants (especially lower‐skilled or irregular migrants) and many suffered loss of income or employment during 2020.

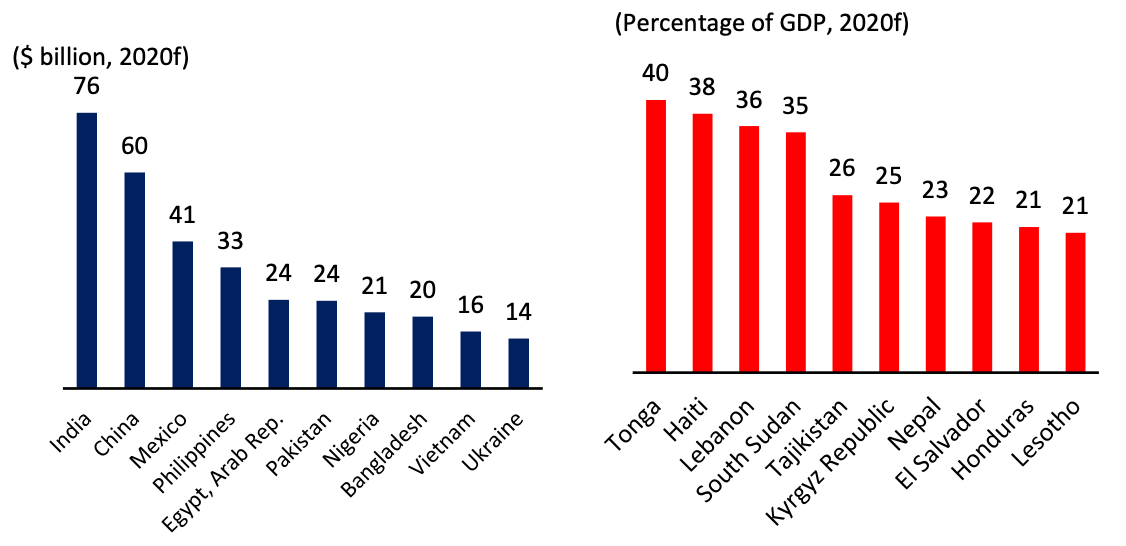

This chart shows the Top Remittance Recipients in 2020 in blue; along with Remittance received as a % of GDP in red. Source: World Bank

But, what is remittance? Who are the senders and receivers of this money? Why are so many families in developing economies dependent on relations who have migrated to richer countries to work and send up to 20% of their earnings back home to support them?

REMITTANCES - the local impact

At a macro level, remittances have a positive impact on both economic growth and poverty reduction, depending on how reliant the country is on foreign remittance flows. In some countries they are 3 times more important to the local economy than foreign aid. (UN) A significant number of small islands and countries with small populations and economies are particularly reliant on remittances. Such is the case in Cape Verde, Comoros, Montenegro and Tonga (as shown in the chart above).

It is estimated that 75% of remittances are used to cover essential things: put food on the table and cover medical expenses, school fees or housing expenses. Also, in times of crises, migrant workers tend to send more money home to cover loss of crops or family emergencies.

The remaining 25% of remittances– over $100 billion per year – is either saved or invested in asset-building or in activities that generate income, jobs and transform economies, in particular in rural areas.

RECEIVERS - the families back home

About one in nine people globally are supported by funds sent home by migrant workers. This equates to approximately 800 million people.

A large portion of these remittance receivers are unbanked or poorly served by regulated financial institutions, particularly in rural areas, which receive 40% of total remittances.

The impact a remittance payment has on a family depends upon its frequency, the amount received and how dependent the family is on this income. In most cases though, it is an additional source of income, which in many cases can represent up to 40% of their household income.

MIGRANT WORKERS

The World Bank states that the average remittance transaction from OECD countries is between USD200 and USD300 and is sent by a migrant worker 11 times a year.

Money sent in-country (like from the city back to a rural community) is much less regular and these transactions average between USD50 and USD150 each.

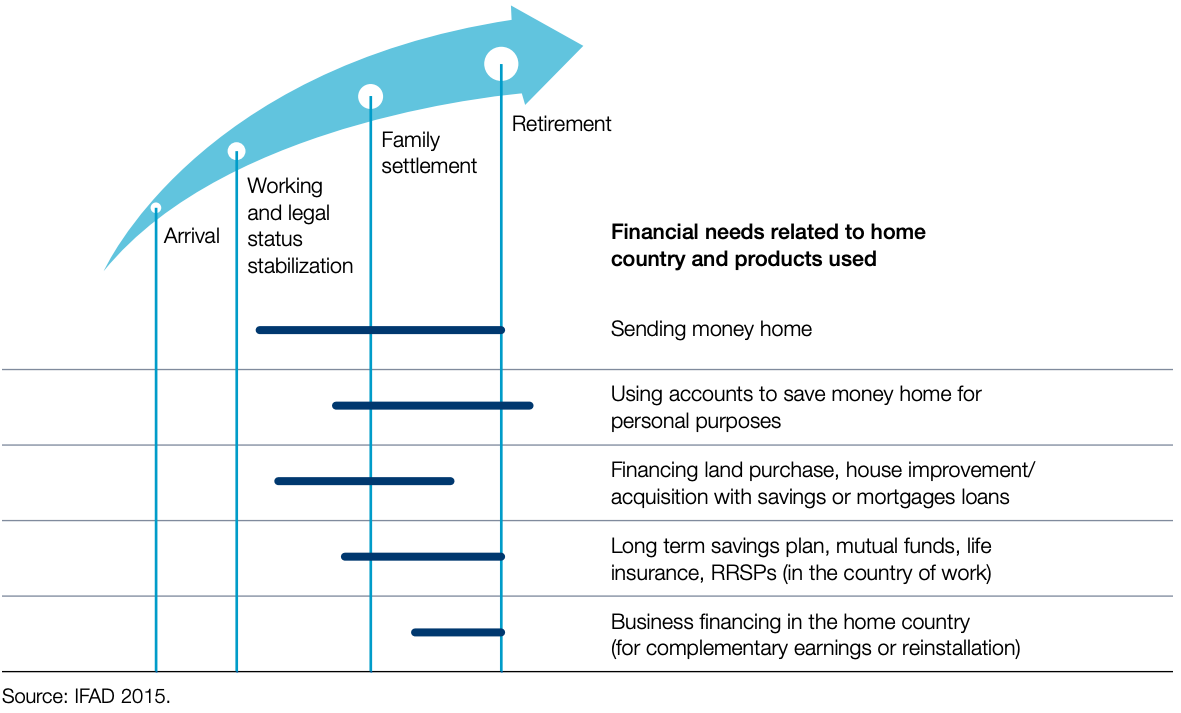

The financial needs of a migrant worker will evolve over time but it is a fact that their needs are determined by personal financial goals. A recent IFAD report states that “The most important need stated by migrant workers is to be able to remit money to their families in a secure manner, quickly and at affordable costs.”

Therefore, affordable remittance transfer services and a secure place to save are essential for the lower-income migrant worker. - Higher-income workers will also demand financial products such as remote bill-payment and long-term savings plans; or even more sophisticated products like housing loans and retirement saving schemes, entrepreneurship loans and insurance products.

These financial needs will change as migrants settle in a host country on a longterm basis - and may even extend to financial products such as mortgages, retirement planning, insurance for body repatriation and family health.

Migrants' financial needs and behaviour evolve as they settle in the host country. Source: IFAD

The reality is that financial exclusion is still hampering the achievement of their financial and migration goals:

- Up to 30% of migrants still use unregulated methods to send and save money. This carries the risk of embezzlement or even robbery.

- A preference for cash-to-cash remittances still prevails, even though regulations are more stringent for in-cash operations, resulting in financial institutions, especially banks, being ever more reluctant to manage in-cash transactions.

- Migrants try to monitor family expenses, organise the purchase of goods and pay for bills remotely, which can cause a lot of issues and funds going astray. These cross-border transactions could be much better served through the use of online platforms that combine cash remittance and direct remote payments for items such as utility bills and school fees.

- Even the most educated and wealthiest migrant workers are obliged to deal with multiple financial institutions to find a combination of products fitting their needs, and often need to send remittances home through MTOs or even unregulated channels.

In order to cater to a migrant's needs, financial service providers should be able to offer an array of suitable products – ideally accessible both in host and home countries - but in reality we know that most of these financial needs remain unmet by traditional financial services providers.

What the sector really needs is support for a range of technical innovations, in particular mobile technologies, digitalisation and blockchain which can fundamentally transform the sector, coupled with a more conducive regulatory environment.

THE FUTURE LOOKS BRIGHT

At Pipit we have the opportunity to work with a number of exciting and dynamic merchants and payment partners from developing economies who understand the basic financial needs of migrant workers, the communities they come from and their own families.

Companies such as Flutterwave, Cellulant and Wari have seen that existing financial institutions and services do not meet the needs of these people in meaningful and localised ways.

They have in effect leapfrogged existing and inflexible traditional financial services, by developing new financial technologies which combine mobile and digital technology with a recognition of the important function that cash plays in these economies, and are leading the way with an array of efficient, low-cost mobile money solutions which meet the financial needs of both migrant workers and their families, whether they need basic money transfer options, cross-border bill payment platforms, or savings and mortgage loan accounts.

At Pipit we believe that as developing nations look at ways to bring Financial Inclusion to all their citizens, they must remember the importance role that cash holds within financially excluded communities and new financial initiatives should seek to conserve the use of cash and work to bring down the global cost of cash transactions for people in developing economies and for those who choose to use cash as their preferred method of payment.